Fuchs (2018), "The Online Advertising Tax: A Digital Policy Innovation" (Vol. 1, CAMRI Policy Briefs). London: University of Westminster Press.

The author proposes new ways to address the increased public criticism of large digital corporations' low tax contributions. In particular, this policy brief introduces a new possibility and policy innovation for taxing online advertising.

In particular, they shed new light on the question how to establish models for taxing online advertising and digital cor-porations. Drawing on Christian Fuchs’ theory of digital labour, their brief stresses that only human labour creates value and that on digital media the boundary between value-production and commodity consumption has become blurred. Policy measures for taxing transnational corporations, including digital companies, need to be based not just on the question where and how much value is produced, but also on the question who produces how much value. Introducing an online advertising tax is an ideal financial foundation for supporting the creation of public service Internet platforms and civil society Internet platforms/platform co-operatives.

The brief makes the seven following proposals:

1 – Tax Models Based on a Humanist Labour Theory of Value: Taxing transnational corporations, including digital companies, should be based not just on the question where and how much value is produced, but also on the question who produces value

2 – Establish a Model for Taxing Online Advertisements: Online advertising should be taxed based on the assumption that users create the value of an online advertisement when they click on it (pay-per-click-model) or when they view adverts (pay-per-view-model)

3 – Create and Fund Public Service Internet Platforms: Legislation should enable public service media to offer advertising-free online platforms so that a public service Internet can be created is needed

4 – Stronger Enforcement Mechanisms for Financial Authorities: An online advertising tax should go hand in hand with strengthening the resources of the financial authorities so that these are able to effectively deal with the increase in monitoring and administration required

5 – Base the Definition of the ‘Digital Permanent Establishment’ on a Humanist Labour Theory of Value: In order to determine standards for taxation, one should always ask: What is the commodity involved? What is the labour that creates the commodity’s value? In which jurisdiction is that labour located at the point of value-production?

6 – Use Models of Digital Value Creation for the Legal Defini-tion of Digital Permanent Establishments: Digital platforms act as constant capital. Users produce data that is valorised in the form of personalised adverts. For each advert that is shown on a profile and the gets clicked upon, one can determine in which country the value-generating view or click took place

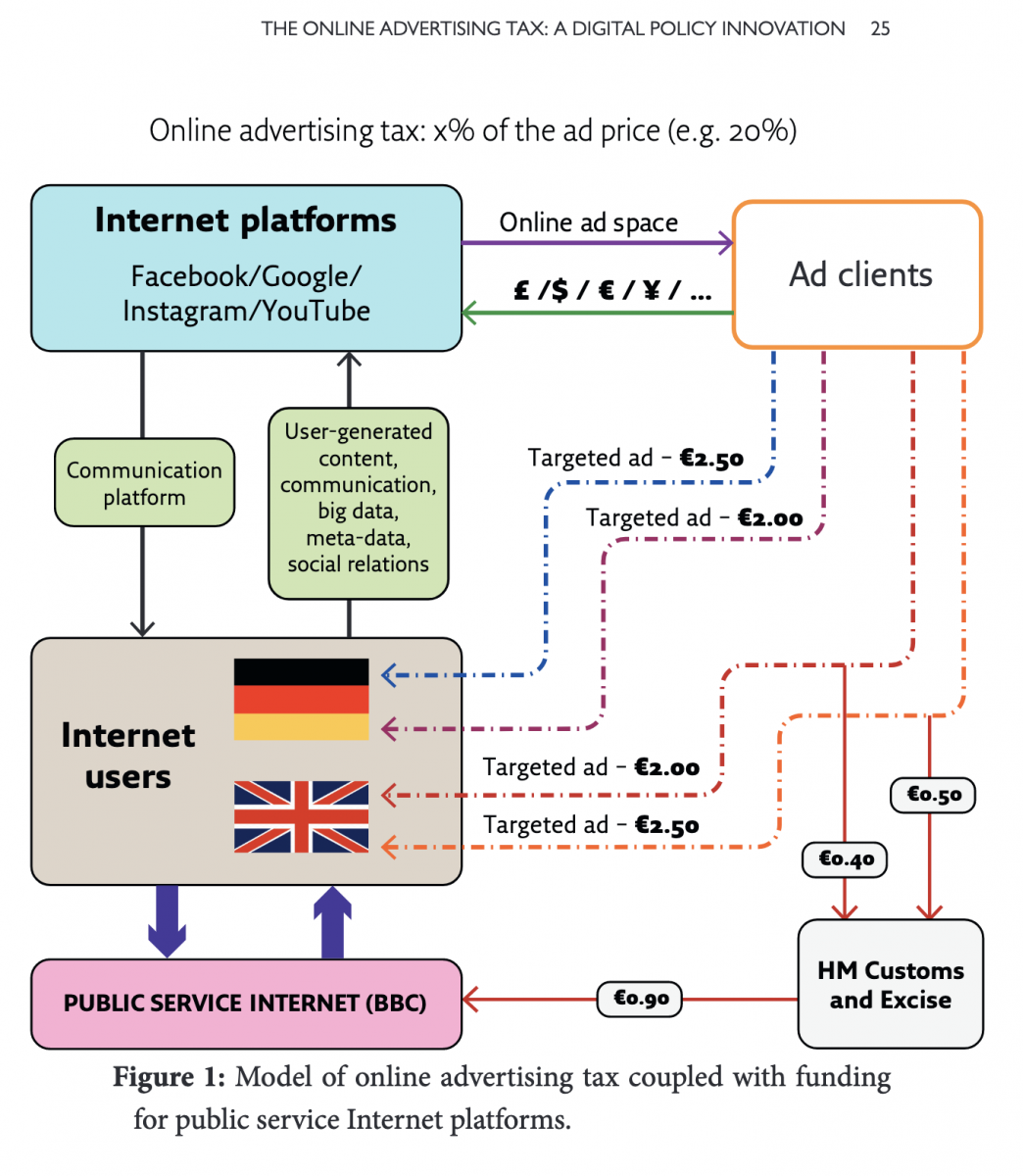

7 – Use the Revenue Generated by an Online Advertising Tax for Financially Supporting Alternative, Non-Profit Internet Platforms: An alternative Internet can be advanced in two ways: by public service media (PSM) organisations and via civil society. Public service Internet platforms operated by PSM can be funded out of an online advertising tax. The model visually represented in Figure 1 presents an online advertising tax with a hypothetical 20% tax rate on advertising